Insurance Costs in Key West: What Every Buyer and Seller Must Know Before Closing

What do flood, wind, and hazard insurance cost for a Key West home?

In Key West, total annual insurance costs for a single-family home typically run $12,000–$17,000, combining flood insurance (averaging $3,000–$8,000/year in Zone AE, up to $20,000+ in Zone VE) and wind/hazard coverage ($8,000–$12,000+/year). Costs vary significantly based on flood zone designation, elevation above base flood elevation (BFE), construction type, and whether a home carries an assumable FEMA flood policy. A wind mitigation inspection can reduce premiums by $2,000–$5,000 or more per year.

By Jimmy Lane | June 23, 2026

The number that surprises most buyers coming to Key West from the mainland isn't the purchase price. They've seen the listings. They've done the mortgage math. What catches them off guard is the insurance bill — and it's big enough to change what they can afford to buy.

A local news story that ran in December 2025 put it plainly: soaring flood, wind, and property insurance costs in the Florida Keys now rival monthly mortgage payments. I've watched it happen firsthand. A buyer falls in love with a property in Casa Marina or Old Town, gets pre-approved, and then gets an insurance quote. Sometimes the deal holds. Sometimes it doesn't.

If you're buying or selling a home in Key West, insurance isn't a footnote. It's a core part of the financial picture — and you need to understand it before you're sitting at the table.

The Three Types of Coverage You Need

Every homeowner in Key West who has a mortgage needs three types of insurance: flood, windstorm (or hazard with wind coverage), and homeowners (hazard). In most of the country, one policy covers most risks. Here, you're almost always buying them separately, and each one has its own pricing logic.

Flood insurance is either purchased through the National Flood Insurance Program (NFIP/FEMA) or through the private market. In Key West, nearly every property in a mortgage transaction requires it — and the cost depends almost entirely on which FEMA flood zone you're in and how high the structure sits above base flood elevation.

Wind insurance can be part of your homeowners policy or a separate windstorm policy, especially for properties in high-wind zones. Monroe County sits in a high-velocity hurricane zone, and lenders require wind coverage. A named storm triggers a separate hurricane deductible — typically 2–5% of dwelling coverage — on top of your standard deductible.

Hazard (homeowners) insurance covers fire, theft, liability, and other standard perils. In Key West, this alone averages $9,835–$25,080 per year, depending on replacement cost and coverage limits. That range is wide because the market is wide — a Bahama Village cottage and a Casa Marina estate have very different replacement costs.

Flood Zones: The Single Biggest Variable

Your flood zone designation is the starting point for everything. FEMA maps Key West properties into three primary zones:

- Zone X — Lowest risk. No mandatory flood insurance for properties outside a Special Flood Hazard Area. Premiums are substantially lower.

- Zone AE — High risk. A 1% annual chance of flooding (the "100-year floodplain"). If you have a federally backed mortgage and you're in Zone AE, flood insurance is required. Annual premiums typically run $2,000–$10,000, depending on elevation.

- Zone VE — Coastal high-velocity wave action. The highest-risk designation. These are properties where wave force during a hurricane compounds the flood risk. Premiums regularly run $5,000–$20,000+/year.

What makes this tricky is that two homes on the same block in Old Town can be in different zones. A house that was elevated during construction in the 1980s may sit in Zone X or carry a much lower Zone AE rate, while the house next door — built lower, unrenovated — may be paying triple.

Elevation Above BFE: Where the Real Math Happens

The number that matters most within Zone AE is how high your home sits above the base flood elevation. BFE is FEMA's published elevation standard for your specific parcel — the height floodwaters are expected to reach during a major storm event.

If your home's lowest livable floor is three feet above BFE, your flood insurance is going to be substantially lower than a home sitting at or below BFE. In Key West, properties built after 1978 are required to have no livable space below BFE — but that doesn't mean every property meets that standard, and it certainly doesn't mean the elevation above BFE is the same across homes.

An elevation certificate documents exactly where your property sits relative to BFE. The City of Key West maintains elevation certificates on file for many properties, and you should request one — or verify that a current one exists — early in the buying process. Before you fall in love with a house and before you make your offer, get an insurance quote based on the actual elevation certificate. The difference between "at BFE" and "three feet above BFE" can be $4,000–$6,000 per year in flood premiums.

The Assumable Flood Policy — A Hidden Negotiating Tool

Here's one of the most underused advantages in Key West real estate: FEMA flood insurance policies are assumable by the buyer.

If the current owner has a long-standing NFIP policy, it may be grandfathered at a rate that no longer reflects current Risk Rating 2.0 pricing. Assuming that policy rather than buying a new one can save you thousands of dollars a year — sometimes dramatically more. The first question I ask about any Key West listing is whether the seller has an existing FEMA flood policy. If they do, we work to transfer it.

This matters more than most buyers realize. FEMA's Risk Rating 2.0 — the updated pricing methodology rolled out in recent years — moved away from flat zone-based rates and toward property-specific risk assessment. A grandfathered policy can carry rates set under the older methodology. You don't want to give that up.

Wind Mitigation Inspections: Worth Every Dollar

A wind mitigation inspection documents your home's resistance to hurricane-force winds — roof shape, roof deck attachment, roof covering type, opening protection (impact windows, hurricane shutters), and how the roof connects to the walls. This report goes to your insurance company, and if your home scores well, the premium reduction can be substantial.

In Monroe County, where wind insurance rates are among Florida's highest, a good wind mitigation report saves some homeowners $2,000–$5,000 or more per year. The inspection typically costs $150–$300. If you're buying, ask the seller for any existing wind mitigation report — it transfers with the home — and build a new inspection into your due diligence if one doesn't exist. If you're selling, getting a wind mitigation inspection before you list can make your home more attractive to buyers who are already nervous about carrying costs.

New Florida Law: What's Changing in 2026 and 2027

Two changes are reshaping insurance requirements in Florida right now.

Starting January 1, 2026, any structure with a dwelling replacement cost of $400,000 or more must carry flood insurance. In Key West, where median sale prices hover near $1 million, that threshold captures almost every residential property. If you're buying a home in this price range and your lender hasn't flagged this, your insurance agent will.

Starting January 1, 2027, all residential structures must carry flood insurance — regardless of replacement value or flood zone. The era of optional flood coverage in lower-risk zones is ending.

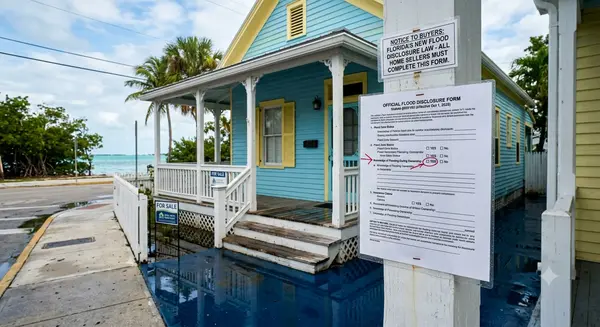

Florida also implemented mandatory flood disclosures effective October 1, 2025. Under Florida Statute 689.302, sellers must now disclose any known flood damage during their ownership — even if no insurance claim was ever filed. The FD-1 disclosure form must be provided at or before the time the purchase contract is executed. This is not optional, and an "as-is" clause does not exempt sellers from it.

What This Means If You're Selling

If you're selling a home in Key West, insurance is part of your marketing now. Buyers are doing insurance due diligence earlier in the process — sometimes before they even schedule a showing. A few things you can do:

Get your elevation certificate in hand before you list. Know your flood zone. If you have a long-standing FEMA flood policy, find out if it's assumable — and market that. Get a wind mitigation inspection done so buyers don't face an unknown. Price your home with the carrying costs in mind: buyers are backing out of deals when the total monthly cost — mortgage, insurance, taxes — comes in higher than expected.

The market in Key West has softened. Days on market have stretched significantly in 2026, and insurance costs are part of the reason. Sellers who help buyers understand and plan for the real carrying cost of a property are closing deals. Sellers who let it come as a surprise after the inspection period are watching contracts fall apart.

I've walked many sellers through the process of preparing their property and their disclosures before we ever hit the MLS. If you want to understand what your specific home will cost a buyer to insure — and how to use that information to price and market effectively — that's exactly the kind of conversation I have before we list. You can also read about the true cost of owning in Key West and what makes Key West real estate a unique investment for more context on how these costs fit into the bigger picture.

The Real Numbers: Running the Full Cost

Let me put concrete numbers on it, because abstract ranges don't help you make a decision.

For a single-family home in Old Town Key West at a $1.2M purchase price:

|

Cost Item |

Estimated Annual Cost |

|

Flood insurance (Zone AE, near BFE) |

$4,000–$6,000 |

|

Wind / hazard insurance |

$10,000–$14,000 |

|

Property taxes (second home, reset at sale) |

$35,000–$40,000 |

|

Total annual carrying costs (before mortgage) |

$49,000–$60,000 |

That's $4,000–$5,000 per month before principal, interest, or any maintenance. On a $1.2M purchase with 20% down at current rates, a mortgage adds another $6,400+/month. Total monthly obligation: around $10,000–$11,000, before utilities.

These aren't numbers to scare anyone. Key West buyers at this price point typically know what they're getting into — or they do after we talk. But they're the numbers you need to know before you make an offer, not after.

Your specific situation will look different depending on your flood zone, your elevation, your coverage choices, whether you can assume an existing flood policy, and whether your property qualifies for wind mitigation credits. That's where the conversation gets specific — and that's exactly what I help clients navigate.

Frequently Asked Questions

Is flood insurance required for all Key West homes?

If you're getting a mortgage and your property is in Zone AE or VE — which includes the majority of Key West residential properties — flood insurance is required by your lender. Starting January 1, 2026, Florida law also requires flood insurance for any structure with a dwelling replacement cost of $400,000 or more, regardless of lender requirements. By January 1, 2027, all residential structures must carry flood coverage.

Can I assume the seller's flood insurance policy when buying a Key West home?

Yes — FEMA flood insurance policies issued through the National Flood Insurance Program (NFIP) are assumable by the buyer. This is one of the most valuable and underutilized tools in Key West real estate. A seller's grandfathered NFIP policy may carry significantly lower rates than a new policy would under FEMA's current Risk Rating 2.0 methodology, potentially saving buyers thousands of dollars per year.

What is a wind mitigation inspection and do I need one?

A wind mitigation inspection documents how well your home is built to resist hurricane-force winds — roof construction, attachment methods, and opening protection. Insurance companies in Florida use this report to calculate wind premium discounts. In Monroe County, where wind premiums are among the highest in Florida, a good wind mitigation report routinely saves homeowners $2,000–$5,000+ per year. The inspection typically costs $150–$300.

What does base flood elevation (BFE) mean and why does it matter?

Base flood elevation is FEMA's published elevation for your specific parcel — the height floodwaters are expected to reach during a major storm event. The higher your home's lowest livable floor sits above BFE, the lower your flood insurance premiums. An elevation certificate documents your exact elevation and is required for any FEMA rate challenge. The City of Key West holds certificates for many properties on file.

Do sellers have to disclose flood damage in Florida?

Yes. Under Florida Statute 689.302, effective October 1, 2025, sellers must provide a mandatory flood disclosure (form FD-1) at or before the time the purchase contract is executed. Sellers must disclose any known flood damage during their ownership — even if no insurance claim was filed. The "as-is" clause in a contract does not exempt sellers from this disclosure requirement.

If you're thinking through these numbers for your own situation — whether you're buying your first Keys property or getting ready to sell — I'm happy to walk through what to expect for your specific home. Reach out anytime.

About Jimmy Lane

Jimmy Lane is a licensed Florida Real Estate broker serving Key West and the Florida Keys. Jimmy has been a full time broker for over 25 years and sold thousands of Florida Keys properties.

Categories

- All Blogs (22)

- flood insurance (1)

- Buyer Guides (1)

- Buyers Guide (1)

- Buying (1)

- Buying a Home in Key West (1)

- Buying in Key West (2)

- Closing Costs (2)

- Costs & Financing (1)

- flood insurance (1)

- Florida Keys Market (1)

- Florida Keys Real Estate (2)

- Florida Keys Real Estate Costs (1)

- Florida Keys Real Estate Guide (1)

- Florida Keys Real Estate Tips (1)

- Insurance (2)

- Insurance & Costs (2)

- Key West (1)

- Key West buyers (1)

- Key West Market (1)

- Key West Real Estate (1)

- market insights (1)

- NFIP (1)

- Seller Resources (1)

- Selling (3)

- Selling / Seller Resources (2)

- Selling a Home in Key West (1)

- Selling in Key West (1)

- Tax & Legal (1)

- Tips for Buyers (1)

- Vacation Rental (1)

Recent Posts

GET MORE INFORMATION